Last year, Bird’s Eye searched for research on average long-term care costs for the purposes of improving our financial planning deliverables for clients. Sam and I have little personal experience with the long-term care system and it was becoming obvious this was a gap in our knowledge. We wanted to address this gap because growing old is something that will affect all our clients.

We didn’t find much, until a fellow Financial PlanningAssociation of Canada (FPAC) member pointed me to this 2022 report from SunLife. While these costs are 4 years out of date at this point, this remains the best resource I’ve found so far. The report breaks costs down by province, and segments by different types of care.

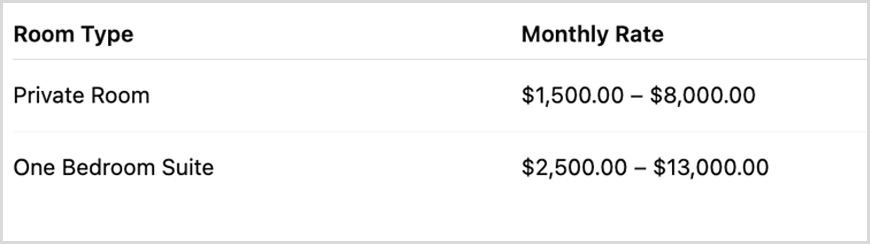

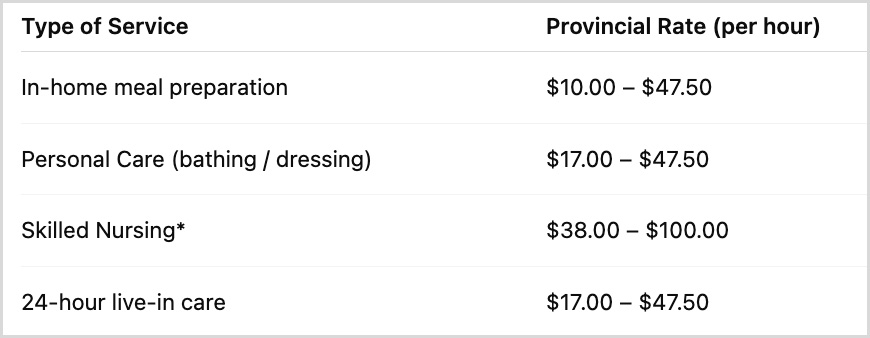

The following are costs for a long-term care home, private retirement home and private in-home care in Ontario, as of 2022.

*Data form SunLife

You can access both the full reports and summaries of each report here.

Even if you don’t intend to use their data in your practice, I believe all planners should read their province’s report if for no other reason than for the wonderful explanations they give for each type of care. If you’ve never had a close family member in long-term care, understanding the options can be a minefield. They also put forward 3 example scenarios of low, intermediate and high care needs. While these examples are just that, it was helpful to see what seniors might need as they move through the stages of retirement.

*Example of low care needs:

- Care plan to assist family caregivers part-time

- Meal preparation - 2 hours a day on weekdays

- Meal supervision - 1 hour a day on weekdays (to include a record of food intake and assistance if patient chokes)

- Personal Care (bathing, dressing) - 1 hour a day on weekdays

- Occupational therapist: to provide initial home safety assessment and recommendations

*Example of intermediate care needs:

- Care Plan to assist family caregiver full days, during the week

- Companionship/Supervision: 3 times a week, 8 hrs a day

- Adult Day Program: 2 days a week

- Safety Supervision: to and from the Adult Day Program - 2 times a week, 30 minutes each way

- Laundry/House cleaning: 3 hrs a week

*Example of high care needs

- Care plan to assist family caregivers full-time, every day

- In-home meal preparation - 7 days a week, 2 hours daily

- Private caregiver - 7 days a week, 8 hours daily to assist with bathing, dressing, toileting and walking and relieve spouse of caregiver duties

- Private Registered Nurse - 4 times a week for 30 minutes to monitor and chart medicine use and blood sugar levels and monitor and change dressing on heel ulcers

- Laundry - 2 hours every other week

- House cleaning - once a week for 90 minutes

- Occupational therapist: to provide initial home safety assessment, recommendations and a 45 minute follow-up after equipment installation

*Data form SunLife

As a firm, we have decided to use SunLife’s 3 need levels and average costs (increased by inflation since 2022) as a template for long-term care in planning. Assuming a life expectancy of age 95, we model 2hours of personal care support a day from age 85-87, 6 hours of personal care support a day from age 87-90, and finally a private room in a private retirement home from age 90 onward, with a sale of the principal residence occurring at that time. We feel that this is a good example of what an average client might need and want. We start factoring these costs into a plan when a client starts talking about planning their retirement date.

To be completely candid though, I’m not actually sure that this is the right approach. This is a constant and ongoing conversation betweenSam and I and we’ve revised our opinions on this matter over time. We’ll probably revise our approach again in the future as we gain more experience and knowledge.

One thing I don’t think I’ll ever change my mind on though is how important I feel this conversation is to have with clients. A one-size-fits-all solution doesn’t exist, and we don’t take that view with anything else in a financial plan, so why should long-term care be an exception? It’s great that we have a resource for average costs, and that we have a template for care needs. But we shouldn’t be using a template at all unless necessary. We need to know what clients want.

It’s true that it’s a tough and awkward conversation. Most of the clients who we’ve started this discussion with try to brush us off, saying that long-term care is not a priority. What we have found is that as clients reach their seventies, their own experience with friends and family starts to inform how they view the level of care they want for themselves.

When a client approaches retirement, and they’re asking,“Can I afford to live on what I have accumulated so far, for the rest of my life?”, not talking about long-term care with them does them a great disservice.

If we omit or lowball long-term care costs from planning at that stage of life, we rob clients of the opportunity to continue to save for it if that’s something they want. Likewise, there are some clients who genuinely are just fine with the most inexpensive, government-subsidized care options. In their case, projecting top-of-the-line care costs does them a disservice too, as it robs them of the ability to spend their money on things that bring them joy. It is our job as planners to help clients think about and plan for the next phase of their lives instead of only thinking about the now; something that comes naturally to many of us but not to our clients.

So if you’re a planner, don’t be afraid to have that tough conversation and push your clients forward a little. And if you’re a client, try to think about what you want the final stage of your life to look like, no matter how far in the future that is for you, because after all it’s YOUR life.

P.S. If you’re a planner and you know of a great long-term care resource we should look at, please send it our way!